Dear Valued Clients and Friends,

The writing of today’s Dividend Cafe was completed Friday morning before the market open, and going into Friday, the market had gone down a thousand points to start the week, then gone up two thousand points in the next three days, to net out a thousand-point gain on the week.

The events that led to the drop on Monday (Presidential jawboning regarding terminating the Federal Reserve chair) and the events that led to the rebound after that (Presidential reversal of said jawboning) inspired the major theme of today’s Dividend Cafe. In short, the Trump market put is not dead. This is an objective opinion devoid of commentary or punditry – it is just a basic statement that questions I, myself, have had about President Trump’s desire for markets to be a validation of his Presidency that has seemingly been answered by numerous events in the last few weeks.

If the “Trump market put” is alive, regardless of whether one believes it should be, a whole lot of other questions about markets still remain, and in today’s Dividend Cafe, we are going to address each of those. So once we have finished our new analysis of the President, we will look at the five big things lingering. Regardless of my assertion that President Trump still wishes for markets to speak well of him, a lot was done over the last three weeks that can’t be easily undone. It’s time to jump into the Dividend Cafe…

|

Subscribe on |

The Psychology of Presidenting

I am more tired of talking about the President’s tariff policies (rapidly changing as they are) than you are tired of reading about them. I am tired of having to explain my place in this current political world (i.e., I do not criticize this tariff ideology because I am a critic of all things President Trump; I criticize this tariff ideology because I am a critic of the tariff ideology). I am tired of the fact that market actors have to not only assess the impact of various policies, but also the likelihood of said policies going by the wayside due to the psychology, pathology, and general read/instincts of the President. It is not a traditional component of macro analysis. But we are where we are.

My view is that more or less everything I have said about the President in the last few weeks (and months) has been correct, even if there have been moments that tested the resolve of these convictions. I believe the President sincerely believes that the U.S. is getting treated poorly in trade deals and that something needs to be done (I disagree with him on this front). At the same time I believe he is an “instinctive” supply-sider (not intellectually, but impulsively) – so believes in the effectiveness of reduced marginal tax rates, deregulation, and energy independence (I agree with him on these fronts, to the point of believing the corporate tax reform of 2017 was one of the most significant pieces of legislation passed in my lifetime). And then I also believe this: The President cares a great deal about his approval, his popularity, his legacy, and his record. While I believe he gets (and has been getting) heavily conflicted advice around this tariff situation, I believe he has pain points at which his natural inclinations, instincts, and willingness to follow the advice of trusted advisors are dismissed.

And through all of this, I think the President’s reversal of April 2 announcements, his waivers on aggressive China tariffs for select industries and products, and his other moderations of aggressive tariff pronouncements all come from the same place… a regard for reputation. I do not expect a smooth lineup from here. I do not believe there is great clarity on how this situation with China will be resolved. I do not think markets are out of the woods. I just believe that a significant driver of where things are headed is the President’s pathology, and this aligns with wanting markets to validate him and his policies. This, all at once, makes day-by-day market projection impossible, but the further-out outcome more predictable.

I believe President Trump is sincerely upset with Chairman Jerome Powell (Federal Reserve head), and I doubt the President feels the same as I do about the impropriety of executive branch interventions into monetary policy. His claims Tuesday that he “was never considering firing Jay Powell,” a couple of days after openly considering firing Jay Powell, speak to the psychology above, not an ideological commitment to central bank independence. His statement this week that he may lower tariffs on China as we negotiate, or exempt automakers, or make other modifications, all speak to this psychology.

I am positive that I will miss things between now and the eventual ending of this tariff escapade, just as I know that those in the administration, themselves, do not know how this is all going to play out. What I believe, though, which happens to be a lot easier to feel conviction in than a particular path between here and there, is that the end run here is not something that undermines the President’s approval. Keeping this long view is likely to aid investors in the avoidance of a lot of bad ideas.

Five Things to Focus on

As we get ready to wrap up the month of April, certainly a historical month in the markets, a refresher on the major things I believe investors face is in order. Each of these things has a slightly different context in late April than they did in early January, but here are the major categories we’re going to unpack:

- Valuations

- AI Capex and Utility

- Tariffs

- Tax bill

- Monetary Policy

#1 Valuations

This is different than the point I was making on valuations at the beginning of the year, and even throughout 2024. The updated issue here is more about the E than the P/E – that is, the idea that the way earnings growth expectations were being priced was already excessive, and now, with a vulnerability to that earnings growth itself, the valuation seems even more problematic. The last eight months of 2025 are far more likely to be about what earnings level is sustaining stock prices than whether or not the market can hold at 22x, or 20x, etc. Excessive valuation is a real issue even when earnings are high, growing, and growing in line with expectations. But when earnings themselves are called into question, valuations tend to pile on the math. This concern may not come to fruition, even for the big tech firms that are most vulnerable. But it is a very key market story going forward.

#2 AI Capex and Utility

While the public policy scene has us focused on tariffs, a deal with China, recessionary fears, and the fate of a GOP-led tax/budget/reconciliation bill, a significant unknown lingers in markets, and that is the unknowns around the commercial utility of artificial intelligence and the capital expenditures that have gone into the space thus far (and are baked in to happen for the foreseeable future).

Seven companies accounted for 27% of the total S&P 500 capital expenditures in 2024. Care to take a guess at who those seven companies are? Yes, the so-called “Mag 7″… And yet, their free cash flow has gone from growing +50% y/y to now declining -3% on the year. The basic narrative for some time has been that some hyper-scalers enjoy huge stock appreciation because they are investing so much in AI, and that AI/semiconductor/infrastructure companies are appreciating because hyper-scalers are investing so much in AI – a circularity that has always posed an outsized risk. I have long wondered if the return on this investment was really all that well understood (by those making the investment, or those benefitting from it). A lot of talk has surfaced about the unknowns adjacent to this – data center investment, for example – but the fundamental concerns remain whether or not both sides of the AI story are vulnerable (the investment for those spending the money, and the continued order flow for those receiving the money).

I doubt this question gets resolved in 2025, but it may very well pose new questions for markets. One of the largest capital investments in history is underway without the ROI of that investment (or the source of that ROI) having been identified. This does not mean it will all go awry. It does not mean there will not be an ROI. It means there is a major “invest first, ask questions later” initiative playing out, and I find it nearly impossible that, even with a happy ending, it does not create surprises along the way.

#3 Tariffs

I will not waste your time this week repeating that “there is a lot on the line” in what happens with U.S. tariff policy (mostly as it pertains to China, and to some degree in eliminating the tail risk of those April 2 announcements coming back).

The buzz this week that contributed to the mid-week rally centered on comments from Secretary Bessent, who said that the current situation with China (no trade, 145% tariffs, and a shutdown of activity) is unsustainable. That’s not exactly news (I know hundreds of small business owners who agree and are aware of tens of thousands), but it was reassuring to hear a sober voice from the administration not pretend otherwise. Seemingly long gone are the days of people saying things like “trade wars are easy to win” and “China will come begging us for a deal.”

The President’s posture has been encouraging, with him indicating multiple times to the public (whether it’s true or not) that conversations are ongoing and he is confident a deal is forthcoming. Additionally, a slew of exemptions continues to be presented, further indicating the administration’s new awareness that the damage being done is significant. Bloomberg reported last night that China is considering exempting tariffs on medical equipment and industrial chemicals, but there has been no formal announcement yet.

At the same time, it seems very clear that China is driving this process (as the President said, “it will depend on China how soon tariffs can come down”). China seems to be going out of its way to insist that no bilateral talks are underway. China’s public posture is that the U.S. must rescind tariffs before de-escalation talks can ensue.

Here’s what is more important right now than a deal with China: the level of economic damage already done (or about to be done) from uncertainty, declining activity, reduced order flow, and general decline of trade and productivity. While traders and media headlines appear more focused on a tweet here and a comment there, and some indications around deal-making with the countries involved, my focus is far more on the economic impact of what has already happened.

Cargo. Freight. Shipping. Capex. Durable Goods. Manufacturing output. New hiring. Hapag-Lloyd announced this week that 30% of shipments from China to the U.S. have been fully canceled. Are U.S. shelves in stores about to reflect this? Steel prices are up 25% since this began, even though other commodity prices are down (i.e., higher input costs, lower growth expectations).

The activity of April and May matters most right now – not deals that may be announced in June or July (and certainly not announcements regarding activity of February and March, all from before April 2).

The underlying tensions here for markets remain:

- We do not know how it will end

- There is economic damage being done along the way, even if it does end

- The assumptions that underlie this policy are deeply flawed (i.e., trade deficits are bad)

BUT,

- The Trump market put appears to not be dead

#4 Tax Bill

This was covered enough last week, but let me reiterate the market considerations that I think are most important at this point, trumping the various political and administrative details that get most of the attention (that is, if this story gets any attention at all these days) …

- There is 0% upside to markets in a temporary extension of the 2017 Trump tax cuts. That outcome, and then some, is fully priced into markets.

- There is 0% (or something very close to 0%) upside to markets even in a permanent extension of the 2017 Trump tax cuts. That outcome, and then some, is fully priced into markets.

- There is a big downside for markets if A or B were not to happen. Of course, markets from the night of Kamala Harris’s concession speech immediately took it as a lay-up that a Republican President, a Republican Senate, and a Republican majority House, all acting with the ability to legislate with a mere simple majority, would not be sunsetting the signature tax bill of the very same President who just got elected. It just is not news to extend those tax cuts – that is supposed to be the political equivalent of the sun coming up.

- There are political ramifications around some of the other tax components that may be a part of this (no tax on tips, modified overtime wage taxation, SALT deduction cap increases) – but limited market ramifications. Limited is not the same as zero, though.

- Any final tax bill that reduces the marginal corporate tax rate (unlikely), that modifies the effective corporate tax rate (much more likely), that enhances deductibility of business expenses, and produces incentives for capital investment will be a pro-growth, supply-side, market boost. This is question #4 in this week’s Dividend Cafe. This little letter E… not letters A-D. Letter E. Mr. Market is going to skip ahead in the book to Letter E and be far less animated by letters A through D, unless something goes wrong.

#5 Monetary Policy

A week ago, the elephant in the room was whether the President would poke the bear and potentially create a Constitutional crisis by firing the Federal Reserve chair over a mere disagreement on monetary policy. Tragically, his own National Economic Council Director appeared to indicate that they believed there was a legal basis for doing so. A few days later, this was dramatically walked back, and now we are back to the good old days of just fighting over what a bunch of academics think we should all charge each other to lend and borrow money. Good times.

The reason this point lingers on my list is unrelated to the drama of a week ago (now), and it is unrelated to downside concerns over “whether or not the Fed loosens monetary policy enough.” I am confident that markets believe we are looking at 75-125 basis points coming out of the Fed funds rate (that is, between three and five cuts of 25 basis points each). We can just meet in the middle and call it four cuts, 100bps. I am confident that this range will happen, and that anything within this range and within this timeline is all “good enough” for markets. It essentially is not a big deal for stock prices unless it doesn’t happen, and I am confident it will.

So why is monetary policy on this list?

If we were not entering a recession, increasing accommodation in monetary policy while the economy is healthy is essentially one of the most bullish predicaments for risk assets. It doesn’t happen often, but when it does, the results have generally been overwhelmingly favorable for risk assets. So this puts two monetary considerations on the table:

- What if monetary policy is looser than anticipated, because economic conditions are worse? Not good.

- What if monetary policy is as loose as anticipated, but economic conditions do not worsen? Likely good, right?

Both A and B are tails – the status quo baseline case is still the scenario currently forecasted – 100bps of cuts, but a softening economy. How the economy unfolds this year in its nexus with monetary policy presents possibilities in markets that we plan to watch closely.

What if we face the end of the world?

The rapid collapse of markets in early April brought back memories of other rapid and significant market declines, serving as traditional fodder for those sociologically wired to worry that “this time was different” and ponder some derivative of “what if this is the end?” Of course, many who do so are just career grifters and peddlers, but I am not referring to these professional permabears. I am rather talking about genuine human beings who are wired to worry.

Many may feel that the President’s aforementioned walk-back from some of his April 2 intentions and the various other “exceptions” and “waivers” and “reversals” since then have all taken that far left-tail risk out of the equation. I do not know if the worst of this market drama is behind us or not – it very well may be. But I do know that any time a traumatic market event takes place, it is well worth re-visiting my gospel of investing for the end of the world (taught to me by the great Howard Marks):

- We can’t predict the end of the world

- We wouldn’t know what to do even if we knew the world was ending

- Anything one could do to prepare for the end of the world would be disastrous if the world didn’t end up ending

- And you may have noticed, the world usually doesn’t end

In 25 years of professionally investing and covering the many decades before that I have historically studied I have yet to come across a perma-bear investing strategy that didn’t annihilate those who were afraid of being annihilated. Now I know, I know, “this time is different” (or, “the next time might be”) – but the four points above, understood in order and holistically, ought to serve as a guiding light in those moments of vulnerability.

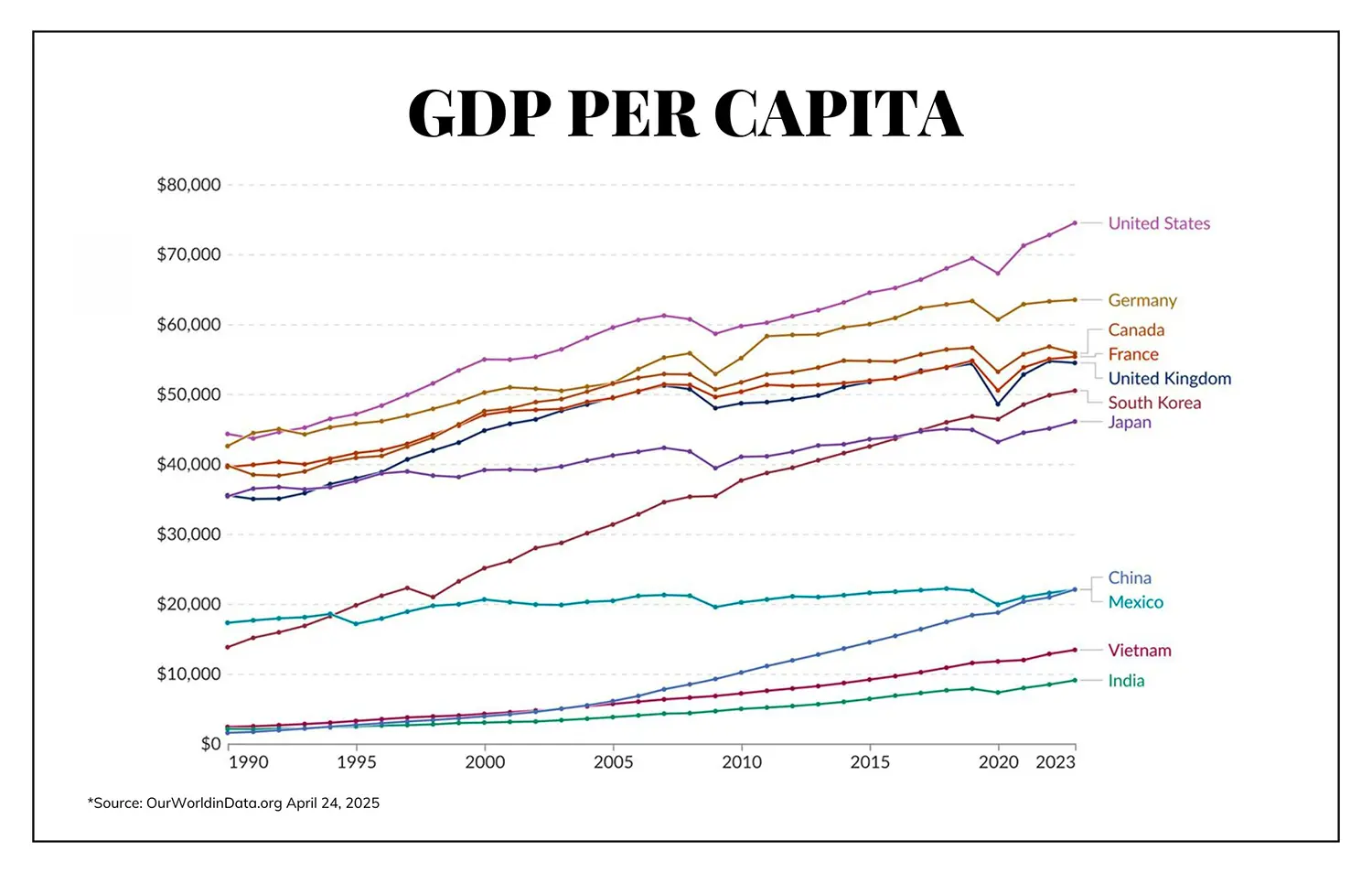

Chart of the Week

It does not appear that things are going that well for the countries “ripping off” in trade deals, or that things are going that poorly for the country “getting ripped off.”

Quote of the Week

“Imagine how much harder physics would be if electrons had feelings.”

~ Richard Feynman

(he certainly understands that physics and economics are different, as economics involves humans, and humans do, indeed, have feelings)

* * *

From the psychology of the President, to the persistence of a Trump market put, to the five things we continue to watch, to basic principles for the end of the world, I hope you got your money’s worth with this week’s Dividend Cafe. To our beloved clients, please reach out with any questions about how any of this is manifested and applied in your own custom portfolio and plan, any time. To our other readers, I hope it is useful information as you or the person you pay for advice guides you through all of this. If we can be any kind of resource, do not hesitate to ask.

And as for what next week holds, my prayer for you is that it will involve peace and joy, no matter what markets are doing. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet