Dear Valued Clients and Friends,

This is a special Dividend Cafe but one that I think will have something for everybody. It speaks to a mentality and a framework that has more than just economic ramifications. It was inspired by a conversation I had with my wife on Wednesday night about some other things, and as our conversations often do, led to another track that led to another track that led to this inspiration for Dividend Cafe.

At the end of the day, investor behavior will always be the primary determinant of investor outcomes. And investor behavior is deeply tied to how one views the “last dollar on the table.” In fact, even outside of one’s investing life, their view of the “last dollar on the table” is likely to be highly relevant to the outcomes and experiences one will have.

One might even argue the “last dollar on the table” is the most expensive dollar one could ever pursue – financially and otherwise.

Let’s jump into the Dividend Cafe.

|

Subscribe on |

Not burying the lede

Let me get the conclusion out of the way. Investors will cost themselves a lot of money if they obsess over making “the last dollar” possible. Investors who adopt the understanding that such things are (a) Unknowable and (b) Unhelpful anyways will be substantially better off. Great mistakes are made when one forgets this or operates from a vantage point that a “max profit” is ever knowable in any other vision besides the rearview mirror.

But actually, there is a lot more to what I want to say today.

That guy

I have been a part of a lot of business negotiations in my adult life. Some have gone very well. Some have not. I have facilitated, observed, or somehow played a part in many, many other negotiations (as an advisor or intermediary). I feel that I speak from some degree of expertise and experience here … there are some people who transact in the business world with a certain, shall we say, “zeal” to get the very last dollar that is on the table. You can call it greed (it may be, but it also may not be). You can call it pride (I think it usually is). And you can call it fear (I am not sure this is always that different from pride). But either way, everyone wants to get the best deal they can for themselves, yet “that guy” I am referring to is someone who would blow up a $20 million deal over a $2,000 expense. “That guy” is going to “get his.”

What I am not saying – read this paragraph fifty times if it will help you not misunderstand

If it takes you 50x of reading this to not email me with a grotesque misrepresentation of what I am saying here, chances are the 50th time didn’t help either, so I will just let my yes be yes, and no be no. I am not saying that someone should enter into any transaction, or do any financial dealing as an investor, buyer, seller, businessperson, customer, or anything else, divorced from self-interest and savvy regard for their own predicament. I do not believe market transactions are charitable affairs, and I actually believe too much of a cavalier spirit in one’s business affairs can be distortive to markets (though thankfully, our individual transactions are not usually at a sufficient “scale” to be that distortive).

I believe in the rule of law. I believe in private property. I believe in buttoning up deals. I believe in having vigorous lawyers and accountants who do their jobs. I believe in a proper alignment of one’s position with their overall interests (and the interests of their family, employees, etc.). And I believe in a theology of abundance within a world of scarcity. I believe in all of these things and have dedicated my life to the advocacy of a free society and market economy.

But, there is a mentality I am describing that has absolutely nothing to do with any of this. And for those who believe the binary choice is either being “that guy” or else laying down and taking a bad deal, you simply are not understanding the domain that most of life exists in – the domain the book of Proverbs was written for – the grey that exists between black and white – the simple mental framework that holds in tension the simultaneous ability to advocate for self-interest and have the total release of the “last dollar.”

C’est la vie

I freely confess that I am more comfortable with the tensions I am writing about in this Dividend Cafe than one who may not yet have financial freedom or abundance may be. But if I am being honest, I do not think I am writing about a release of the last dollar that should happen once you are financially comfortable. I am actually arguing that it is a lot easier to become financially comfortable when you have released the last dollar.

The mentality that advocates fairly and effectively but accepts the simple truism in life that “what goes around comes around” – and that one just never really knows exactly how the bio-rhythms of the universe will blow – is a far better-positioned mentality for the realities of economic life, not to mention the specifics of investing life. This is not a case for karma – it is an empirical observation that people who actually know how the world works know that some fights over the last dollar cost people many, many more dollars in a lot of cases.

A “c’est la vie” attitude may seem too cavalier, but if I had to critique one extreme or the other, it would be the side that believes they can bully, fight, grind, obsess, or haunt their way to every penny. Man plans, God laughs.

Dude. What are you saying?

How many real estate transactions have blown up because of a difference over X, only for that seller to have to sell later for way less than X months or years later? If I could write a book one day on the things I have seen clients tell me over the years about real estate they own versus what ended up happening (or worse, NOT happening) transactionally, all six of the people who would read that book would be horrified!

If you could fathom how many individuals went for a mortgage that was 1/8th of a point less than another option, only to forfeit service, touch, and needed care in the process or post-transaction, you would be blown away by the dollars in the universe we are talking about that have been lost, even though someone thought they were found.

I am saying that in our day-to-day lives, there are times when obsessing over the last dollar can cost us money. A humble juxtaposition of wisdom, serenity, diligence, and stewardship is not only best for our emotional well-being (I think the cool kids these days call it “self-care,” which is adorable) but also for our financial condition.

More and more of the big boys and girls get this

For those of you familiar with the vernacular of commercial real estate, consider the benefit of cheaper borrowing costs from the CMBS market versus a relationship lender, only to see the terms, covenants, and customized needs of a situation blow someone up when a more bespoke credit solution was needed later.

We are heavily invested in the private credit space, which can include direct lending in the middle market. Lately, more substantial borrowers (upstream from middle markets) have gone to the private credit markets versus the high-yield bond market or syndicated bank loan world, paying 200-300 basis points more for the “privilege” of doing so. Why would they do this? Quick access, privacy, intellectual capital, strategic resources, any number of things. A broad and rounded set of interests trumps the “last dollar” – and yet does so perfectly within the paradigm of pragmatic self-interest.

The most successful business people I have been around for many, many years now have routinely done deals with one who was not the highest bidder, factoring in a vast set of intangibles that trumps their obsession with the “last dollar.” This observation has been so universal in my experience that I consider it normative.

Investing 101

We expect to lose money every time we re-balance a portfolio or trim a position, and we do this knowing that this is our explicit expectation. What in the world did I just say?

First of all, if we have a stock we bought as 3% of the portfolio, and it grows to 6% of the portfolio from outsized gains, if we believed it was at imminent risk of dropping a lot, why would we trim it from 6% back to 3%? Wouldn’t we sell the whole thing if we believed that? Yet, if we believed it was likely to continue growing and performing, wouldn’t we want to keep it at 6% to capture those “last dollars” of ongoing growth?

See, the answer is, “We rebalance to the right weighting for that stock because we are not in the business of knowing what every stock price will do and when, and we have accepted that receiving the last dollar of gains on a given position is unnecessary in the broad objective of achieving financial goals.” Re-balancing is a conscientious decision to forego a last dollar for the purpose of risk management, balance, and optimal portfolio management. It accepts the unknowable and pursues the knowable – that a 3% weighting will still make you money when the stock goes up, and a 6% weighting will hurt more than you want if things go south. (I use those numbers for purely hypothetical and illustrative purposes).

Staying within a zone of volatility that does not threaten your peace of mind, or your leverage ratios, or other important parts of your financial and personal profile, is the hallmark of a successful investor. Pursuing the last dollar is contrary to staying within a zone of volatility. And then thinking you can trump it all is the hubris that becomes fatal.

FOMO is really about a “last dollar mentality”

As I have often said about the reason the Ten Commandments climaxed with “thou shalt not covet,” envy is a much more prevalent sin than greed. Nothing drives worse investor behavior than wanting something because of the fear that someone else is getting something you are not.

Whether it is a Ponzi scheme or a shiny object (or a combination of the two), the thing that has driven so much excess throughout investing history, particularly in this modern era, is the fear of missing out. And people hold on to dynamite past the point of explosion because they cannot bear to let the last dollar go. It has blown up investors who could not believe their own lyin’ eyes about the absurdity of what they owned. And it has done great harm to investors who owned very good companies but somehow believed the “last dollar” was more important than risk mitigation.

I hate the examples I have of this in action – of the inability or unwillingness to potentially leave money on the table ending up doing massive harm. I know some call it greed, some call it stupidity, some call it arrogance – and I am sure some or all of those things are frequently at play.

But I think it is a mentality that can be discarded for a superior one, even if the mentality is not rooted in some character or intellectual deficiency.

Conclusion

Human nature is a failed investor. Human nature can be a failed negotiator, too. And that is never a bigger risk than when one believes their negotiating prowess actually means they are fighting for what is theirs.

All people – borrowers, lenders, buyers, sellers, economic actors, and yes, investors, would do well to remember that, yes, what goes around does often come around, and there really is a universe that seems to spin outside of our obsessive control. I am blessed to be a part of it, but even more blessed to know that I am not spinning it. I certainly have a right and even obligation to make good and responsible decisions. But no, the “last dollar” is not one of them.

I think the most dollars I ever made came from the vastly fewer dollars I left on the table before, on purpose.

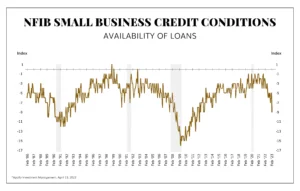

Chart of the Week

Loan demand. Credit availability. Inflation. The Fed. All of these things overlap in the Venn diagram of our economy. And credit markets are telling us that one of these things is not reading the others very well.

Quote of the Week

“If people looked up their dividend income every 90 days instead their account values every 90 minutes, they might just become markedly more successful investors.”

~ Nick Murray

* * *

I know it was a little different this week, but I hope its thrust pulled through for you. Its message really does transcend the investing lesson. Don’t be “that guy.” It will make you more prosperous, and I mean that in the most “flourishing” sense possible. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet