Dear Valued Clients and Friends,

I have pretty much written each Friday’s Dividend Cafe on the Friday morning of the day you receive it every single week for over a year now. If there is an exception to that over the last 12+ months I do not remember it. I used to write the Dividend Cafe in bits and pieces throughout the week and then “pull it all together” on Friday mornings, but a little over a year ago I changed my approach and I have been happy with the results.

Well, this week taking advantage of the Monday holiday and some extra peace and quiet in the very early morning hours of a day that the market was closed, I wrote what would maybe be half of a Dividend Cafe on the subject of capital, liquidity, and interest rates. I loved where it was going and felt it was a good base for a needed Dividend Cafe on a crucial subject at this point in time.

And yet, here I am on a Friday morning, with images of Russian rockets striking all over the Ukrainian capital of Kyiv on my television set, and I am not even opening the draft of that work from Monday morning. Yes, I will be able to use it next week (or at some future date), but this is certainly one of those rare weeks where Dividend Cafe warrants a nod to current events.

Markets have experienced volatility in the build-up to events of this week and in the events themselves, though I would argue it has been much less volatile than I would have expected. The mere presence of market volatility is not the reason to devote a Dividend Cafe to this week’s subject. I don’t much care about market volatility other than the frustration I feel when we don’t get enough of it.

However, our citizenry has mostly decided “foreign policy” is one of those things that mattered from 1939-1989, with a little exception to the rule in the immediate aftermath of 9/11. The relevance of the international order to market mechanics and the cause of a free society has been forgotten, and I think the present situation with Russia/Ukraine provides a good excuse to re-visit the inconvenient world of geopolitics.

So welcome to a Dividend Cafe devoted to Russia/Ukraine, and may your investor knowledge and appreciation of global affairs grow as a result. To that end we work.

First, a little perspective

The Dow closed last Friday at 34,079. At 4:00 in the morning on Friday of this week, it was sitting at 33,224, though futures were pointing down a couple hundred points (and are now pointing up. As we saw intra-day Thursday (markets rallied +1,000 points from intra-day low to closing high), no one knows what a day will bring. This number could be much worse or much better or right in this same range by the time you are reading this, but I don’t have the luxury of writing this Dividend Cafe after the market closes. So as I type, we are down -850 points on the week, or down -2.5%. The Dow is not yet even down -10% from its all-time high (closer to -8%). So far, this is small-ball stuff. If the Dow was down -8% right now after the prior 14-month rally and there was NO war in Ukraine, I wouldn’t even be remotely surprised. It would be “par for the course” market activity.

Admittedly, things have been a little worse in the tech-heavy sectors of the Nasdaq and the S&P 500 (down -17% and -12% from their all-time highs, respectively), but no one can really claim that excess downside is related to Russia/Ukraine. We have gone to great lengths to explain how “shiny objects” needed to be re-priced, and how tighter monetary policy would serve to re-rate expensive P/E stocks.

Stock Market Summary

Three things are true at once:

(1) There has actually been very little directional market impact (in equity prices) thus far from Russia/Ukraine.

(2) There has been a meaningful increase in equity market volatility around Russia/Ukraine.

(3) The directional impact could worsen or improve at any time.

History lesson

Markets were negative intra-day in the first day of global military hostilities in each of the last dozen hostilities, but in nearly every case the markets actually ended “day one” of such hostilities in positive territory.

*Bloomberg, Feb 25, 2022

Okay. What is going on?

It does not seem reasonable to me to conclude that Putin’s agenda is anything less than the overthrow of the Ukrainian government and the occupation of the independent country. There has been nothing “targeted” about Moscow’s aggression, it has been done with no sneaky pretense or propaganda (remember the initial reports that they would attempt to do this behind a “false flag” operation), and it is seemingly being carried out with no concern for the international response.

Speaking of which, do you all know who is president of the United Nations Security Council? I’ll give you a hint – they just launched an attack on Ukraine this week.

Russian military forces are launching rocket attacks on the capital city, and reports are that Russian strikes have taken out Ukrainian air defense entirely.

Sanctions or Gestures?

I think the fundamental tension right now for markets and the major issue around which most economic impact revolves, will be the severity and impact of whatever sanctions are imposed. There is a sanction severity that could very well take the idea of this conflict being protracted off the table (or at least severely limit that possibility). The gray area in all this that politicos, foreign policy analysts, and certainly investment analysts have been unable to decipher is where these things are going to land.

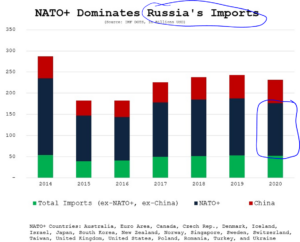

Let’s start with some economic reality. IF (it remains an IF) the NATO+ countries block off exporting goods into Russia, let’s just look at what that means to Russia and its reliance on imports from NATO+ countries:

*Corbu LLC, Feb. 24, 2022

The leverage is there to make sanctions a massive weapon in combating this war effort of Putin’s Russia.

Sanctions Status

We know that thus far President Biden has tinkered around the edges of what sanctions have actually been imposed (targeting a few specific Russian businessmen and banks), but the stakes are about to get much, much higher.

- A far more serious list of export controls are coming (see here)

- While a blocking of Russian banks from the international SWIFT system (international money wires) has not yet been done and needs to be done, and I am reasonably sure will be done, it will be sanctions on Russia’s central bank that makes or breaks their financial mobility.

- A block on Russian energy imports has to be coming at some point – and this has the potential to be the game-changer. I doubt it will come this weekend, but this is the lifeblood of the Russian economy. Yes, it will increase global energy prices. Yes, it will fuel margins in the U.S. energy sector. No, we are not prepared with U.S. energy assets to fully exploit it as we should. But yes, it is the most potent weapon available.

- Putin does have $640 billion in FOREX reserves which buys him a lot more margin than Russia has had economically over the last 30 years. Is he willing to exhaust that? And will the slow degradation of his capabilities over time become relevant? The challenge in handicapping this for markets is that Putin has become so erratic and unpredictable that no one can say for sure (nearly all of the commentary that believed these aggressive acts would not come to fruition were based on rational analysis of Putin acting rationally or with self-interest; that analysis may be assuming things about Putin not presently in play).

- The export controls the U.S. is putting in place on tech products (semis in particular) should prove efficacious, but do cause me to wonder why we were exporting tech IP to Russia, to begin with? The answer is that we mostly weren’t – but rather export tooling and parts to other countries who do export finished products to Russia. This is likely to have a chain reaction effect I am trying my best to monitor.

- The UK has been aggressive in sanctioning banks and capital markets in Russia and stopping Russia from raising debt in UK markets. The U.S. has prohibited secondary market transaction in the Russian bond market. The

- The EU agreed to a ban on aircraft and parts exports to Russia. and a ban on a significant level of technology products and components.

- Back to Energy sanctions … Those resisting the idea of sanctioning imports of Russian oil and gas are concerned with the total global impact on energy prices if such supply was effectively taken off the market. It’s a legitimate concern, but one that can be rectified in other ways if the political will is there. The main question is whether or not Europe is willing to take on short term pain for the longer-term gain of squeezing Russia where it most hurts (i.e. their huge economic reliance on exporting oil and gas)

- And one thing to not lose sight of … once one accepts that Putin is not exactly acting in his own best interests, there is no reason to view the possibility of stopping oil/gas transactions with Russia as a one-way street. He could very well stop exports to hurt Europe just as much as Europe could stop imports to hurt Russia. My own view is that Putin has calculated that Europe’s electricity production and heating requirements need his natural gas more than he needs their money.

What to watch for next

Will Russia take over Kyiv – that is the next question here. If civilian casualties stay limited, and if Russia’s attempts to occupy Kyiv are rebuffed or reversed, there is still an off-ramp. But clearly, that string is very, very thin. De-escalation is the best path for markets and for the nation-state actors involved.

If de-escalation does not soon happen, there will end up being a capitulation. Who the capitulating actor will be remains to be seen, but will have a profound impact on the final conclusion of this (see below).

Some real investment takeaways before the big conclusion below

(1) It is hard to see a scenario where Europe’s economic growth is not impacted here, with the primary question being “how much?”

(2) It is hard to see how all of this does not benefit the energy sector, with both margins and volumes improving to the benefit of the midstream and upstream sectors, both short and longer-term.

(3) Be prepared for ongoing volatility, period.

God forbid we go ten minutes without bringing up the Fed

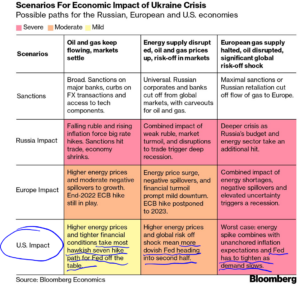

Notice anything in particular here in how Bloomberg this morning assesses the various scenarios for risk and impact out of the Russia/Ukraine situation to the United States?

EVERYTHING is about the Fed. There is an underlying presumption that the lens through which we must view anything impact the economy – even a war in Eastern Europe – has to be in how it may alter the trajectory of Fed policy.

Do I believe there could be some excuse for the Fed out of this geopolitical matter to become more dovish? Well of course, but I have argued they would like an excuse for such with or without this incident. My point is that the singular obsession of financial media with the Fed, and indeed, the singular obsession of many economic actors with the Fed, is not healthy. This is a point I have been trying to make for a long time.

Conclusion

If this conflict is not done within 72 hours, and I have no reason to believe it could or will be, then I cannot imagine a scenario where the final outcome of all this is not either: (a) The end of the Putin regime, or (b) A dramatic shift of the rules-based order.

How does A happen? By the sanctions being so severe and swift (no pun intended) and effective that it leaves him running and with egg on his face. He may not be removed from power, but he would be a feckless and humiliated leader on the world stage.

What does B mean? That the NATO bloc countries tolerate a sovereign nation invading and occupying another sovereign nation, re-drawing the map of the globe, and thereby eliminating the international order that has come to define post-1990 affairs.

I am a sucker for the rules-based order, believing it to be a key tenet of American strength and foreign policy, and would far prefer to see Option A play out than Option B. On the margins, if Option B prevails, I do not believe people or markets will immediately respond. They may even breathe a sigh of relief at the apparent resolution of this conflict.

But no, it will not be good for the long-term expected returns of markets to lose any piece of the international rules-based order. It will not be good for European stability. It will not be good for global peace.

Chart of the Week

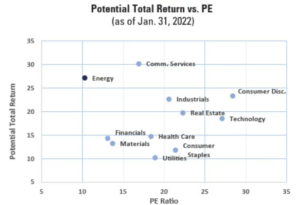

What do you get when the dividend yield plus five-year projected earnings growth is among the highest of any sector, and yet the P/E ratio valuation is among the lowest? You get the Energy sector.

*Richard Bernstein Advisors, Feb. 24, 2022

Quote of the Week

“I am not bound to win, but I am bound to be true. I am not bound to succeed, but I am bound to live by the light that I have. I must stand with anybody that stands right, and stand with him while he is right, and part with him when he goes wrong.”

~ Abraham Lincoln

* * *

I could go on and on here on all of this but I really do need to leave it there. I assure you DC Today will cover more bases next week. In the meantime, enjoy your weekends and appreciate the relative freedom and security we enjoy.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet