Dear Valued Clients and Friends,

In this week’s Dividend Cafe:

- We look at the latest in the soap opera that is the Federal Reserve and the White House,

- And apply it to what to expect for interest rates in the short term (as Kevin Warsh becomes the new Fed chair very soon),

- But most importantly, look at where he sees room to make a real change in monetary policy – less in the real policy rate and more in the use of the Fed’s balance sheet as an economic tool

Let’s jump into the Dividend Cafe …

|

Subscribe on |

All the news that is fit to print

This morning, in the middle of writing this Dividend Cafe, the Justice Department announced that it was dropping its investigation into Chairman Powell and the cost of the Federal Reserve’s building renovation. The reason this matters is that Jerome Powell’s term as chairman is set to expire at the end of May, but the votes are not there in the Senate Banking Committee to advance the President’s nominee for the position, Kevin Warsh, because Sen. Thom Tillis of North Carolina said he would not agree to take up a vote until this legal threat to Powell was resolved.

This morning, the DOJ did just that, dropping the threat of a criminal investigation, saying they had “turned it over to the Inspector General of the Federal Reserve.” What the DOJ neglected to mention was that the Inspector General has now done a comprehensive investigation twice and found no wrongdoing (you may not be surprised to hear that building costs, labor costs, and equipment costs have, ummmmmm, gone higher since 2017 when this project was first approved – before Powell was there). It was Chairman Powell’s position, and that of the Republican Senator from the great state of North Carolina, Thom Tillis, that the investigation threat was a form of lawfare; hence the refusal to move the Warsh nomination forward until the DOJ backed down.

Well, now they have, and the Tillis blockade will end. Sen. Tillis not only never framed his actions as related to opposition to Kevin Warsh, but actually explicitly stated the exact opposite. Tillis (and a perfectly sufficient number on the Senate Banking Committee) are favorable to Warsh, but viewed this blockade as the only leverage they had to end what they viewed as lawfare. With the Tillis strategy now having worked, I expect the Banking Committee to vote this coming week, followed by a quick and full Senate vote shortly thereafter.

In short, I expect Kevin Warsh to be the new Fed chair by May 16.

But Powell?

With Powell’s term as Fed chair legally ending, does this mean he will be gone as a voting member of the FOMC? I believe so, but I cannot say that for sure. People who love Powell, people who hate Powell, and people who have a brain and were raised with the capacity to think for themselves can probably all agree that Powell is an institutionalist, and that the tradition of the institution is that the Fed chair departs when his or her chairship comes to an end. Powell has, understandably, not committed to doing so up until now, saying he would make that decision when the threat of a criminal investigation came to an end. My expectation is that he will honor the tradition of a Fed chair departing so as not to be a distraction to the new chairman. It is the right thing to do, and it is the tradition that has been in place for nearly a hundred years. Powell has done a lot as Fed chair in terms of monetary policy that I disagree with – some of it vehemently so. But I believe (and am essentially certain of this) that he is a good and honorable man. The drama of clinging to a FOMC vote from a departing chair should be averted.

I think.

So where does this leave us?

The prediction markets moved from 31% to 83% this morning that Warsh will be confirmed by May 15. The odds are above 94% that it will be by June 1. So, assume we enter summer 2026 with Kevin Warsh as the new Fed chair and Jerome Powell no longer at the Federal Reserve. I have already made the case as to why I believe Warsh was the right pick to chair the Fed, particularly from the candidates who actually existed. The issue that has changed since the beginning of the year is not whether or not I still like Warsh (I do), or whether or not he will be confirmed (he will be), but rather what market expectations are for interest rate cuts after he takes the mantle.

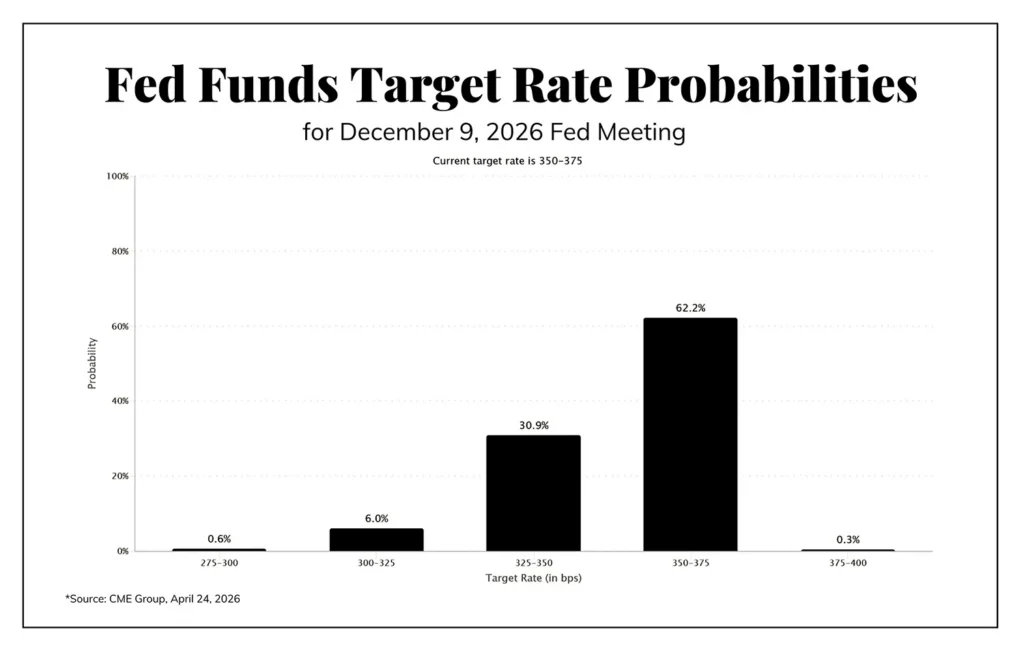

Current expectations are a 62% probability of no rate cuts between now and the end of the year. Yesterday, that was 76%, so the Warsh confirmation approval has already moved market expectations. There is a 31% chance of one rate cut, and almost no chance of more than that.

What changed from the early year expectation of a 3% fed funds rate by the end of the year? Well, oil prices above $90, for one thing. General price impact from the activities in the Strait of Hormuz created an expectation that price stability would trump job vulnerabilities in how the Fed would view the balance of priorities for the rest of the year.

And don’t bet against the futures, right?

This is a tricky one for me because I have spent nearly my entire career saying, rightly so, that the Fed does not dictate the market expectation, but the market expectation dictates what the Fed will do. A better way to say it is that the market expectation already reflects Fed intention, by design, as the Fed has used “forward guidance” aggressively as a form of monetary policy for 20-25 years (Alan Greenspan swore by it).

And I have said this repeatedly – that the Fed generally does not do anything to surprise markets – that they at least “telegraph” in advance changes in plans so as to allow markets to discount activity before it happens. 2022 into 2023 created an exception to that, to some degree, as the Fed started the year indicating a 1.5% rate ending rate expectation (off of 0%) and instead reached 5.5%, but even that draconian tightening came with meeting by meeting by meeting advance notice that their posture had changed. 1994 was a true exception to this, but I would argue it was the aftermath of 1994 (Orange County ought to remember it well) that changed Greenspan’s approach to this.

So, if the futures are expecting the Fed to leave rates alone for the end of the year, that is what we should expect, right?

Not so fast.

First of all, 62% is not 80%, 90% or 100%, and a 30-35% chance is high enough that we cannot accurately say that markets are predicting “no change.” 30-35% in April is plenty high enough to assume we could get one rate cut between now and the end of the year, just based on current fed futures action alone.

But I would also say that the forward guidance tool is, itself, not quite up and running when one chairman is leaving, and another is coming in. A new, not-yet-confirmed Fed chair has not yet met with his colleagues. He has not yet held a Federal Open Market Committee. He has not yet talked to the press about intentions or given a speech at the Economic Club of New York or the Brookings Institution about what he wants to do. In other words, there is a transitional dilution here of the potency of forward guidance and futures market expectations.

Why a lower fed funds rate?

Putting aside what I believe the Fed should do, the case for what they will do involving a rate cut or two between now and the end of the year can best be stated as follows:

(1) It is simply incomprehensible to me that the new chair will not cut rates once at his first meeting after the entire saga with the President and the current chair over that same subject. This does not, in and of itself, imply anything about what should be done – it merely states an expectation that there is a significant reason to believe that such will take place. But …

(2) Beyond the reasoning in point #1, the new chairman sincerely believes that supply shocks to oil are not monetary phenomena (because they are not) and that the current productivity levels allow greater leaning into accommodation versus tightening, given the vulnerability of labor markets. Now, I happen to think that is likely true (for 25 or 50 basis points), but I am not right now saying it as an argument for doing it – I am saying it as an argument for what Warsh will argue – for what Warsh does believe.

But wait, there’s more …

It’s all about QE

My belief that Warsh will argue for, and win the argument for, a slightly lower fed funds rate is connected to the fact that he will not make the argument for such in a Bernanke-Yellen-Powell plea for all-around easier monetary policy. Rather, he will make the argument as one of the barbell – that we can avoid an easing bias in monetary policy even with a lower fed funds rate by applying pressure on the other end of policy tools, that is, the Fed’s balance sheet.

Warsh believes that a productivity boom is going to materialize, which finds its way to the real policy rate (nominal rate less inflation). The focus I believe he is going to bring, not on day one, but over the course of his tenure, is in decreasing the Fed’s role in the total marketplace via its balance sheet. A lower fed funds rate can avoid excess accommodation if coupled with addressing the balance sheet.

Markets being reprogrammed not to expect the Fed to buy Treasury debt issued to fund Congress’s profligate spending sounds like a very good thing to me. But realistically, downsizing the Fed’s market footprint will take time, and there is a lot more to the excessive spending ways of Washington, D.C. than the Fed’s role as a bond buyer.

And one more thing…

One of my favorite macro analysts on the planet, Rene Aninao, has pointed out that regardless of where a reduced Fed bond-buying dependency goes (he is more optimistic than I am about it assisting the cause of fiscal discipline), it certainly improves price discovery and increases foreign participation in our bond market. The Fed’s involvement crowds out the latter and substantially distorts the former. And anyone who believes either of those things is good for economic growth has a very different understanding of economics than I do. A reform of the Fed’s mentality on QE will not, contrary to popular belief, push the long end higher, because it ultimately drives more competition for our bonds, which is organic and healthy, and that puts downward pressure on yields.

Conclusion

If Warsh’s term as Fed chair is to live up to the hype that I believe it could create, he will reverse the excessive interventions of the last two crises and facilitate a healthy deregulation that drives financial innovation, new credit products, healthy competition in a privatized banking sector, and views American capital markets as the wonder that they are – not something requiring the centralized Ph.D cabal of the Fed we have had for the last ~20 years. The Fed needs an institutionalist – someone who understands the importance of credibility – but who does not equate credibility to mere academic papers and degrees. It requires an understanding of markets and, most importantly, of market dynamism, which has been lacking for too long.

Do I think the Fed cuts rates one or maybe two times between now and early 2027? Yes, I suppose I do. But what I care about far more is someone will to at least start the process of changing what we expect of our nation’s central bank. We have expected too much for too long. And they have tried too hard to meet that expectation.

Chart of the Week

Quote of the Week

“Financial markets and the Treasury market are telling us almost nothing about the state of the economy because central banks are influencing those prices with every word, with every nuanced speech from every reserve bank president. We would be better off if markets were setting prices instead of taking their lead from a bunch of government officials seven years into a U.S. economic recovery.”

~ Kevin Warsh, 2015

* * *

I will be back in the Dividend Cafe on Monday with the latest in markets, Iran, the economic data, public policy, and more. It’s not slowing down, and there is much to cover. In the meantime, enjoy your weekends, and reach out any time.

I can’t promise total Fed reformation any time soon. But I can pray for incremental, modest, marginal improvements. My hope is that if Kevin Warsh is reading this he would say, “to that end I will work.”

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet