Dear Valued Clients and Friends,

As I am typing, the market sits at 30,000 exactly on the Dow, really close to 4,000 points higher than it was in the middle of the day on Friday, October 30 (it closed at 26,500 that day). Now, pre-market futures this lovely Friday morning are down 100 points or so, and each minute, hour, day creates new opportunities for an uptick or a downtick, but the point I am making is nothing more than the empirical fact that …

- Over the last 42 days, the market is up very close to 4,000 points

- Over the last 42 days, Joe Biden has won the Presidency

- Over the last 42 days, reported COVID cases have grown

- Over the last 42 days, weekly jobless claims have picked back up

- And once again, over the last 42 days, the market is up very close to 4,000 points

Now, I could write you a Dividend Cafe today reiterating a couple of things I have already written 100+ times in 2020 (and they would be no less valid now than they were then) – that the Fed has implemented monetary policies that have indisputably served to boost the valuations of risk assets … that the COVID doom & gloom in the press has unimpressed markets as markets learned the more detailed nature of the virus’s risk and specific vulnerabilities about seven months ago … that markets are forward-looking and with a vaccine on the horizon see a better 2021 looming … that economic damage has been limited in this painful year to a rather vulnerable but less systemically impactful part of the economy … and so forth and so on.

And if I wrote that Dividend Cafe, I would hope it would be useful, fruitful, and informative in some of the market lessons it would contain. However, it would very likely miss the most important thing one could say about this market, and frankly, one of the most important lessons one can learn about the nature of capital, period.

So that is the ambition of Dividend Cafe today. To explain why the market has been behaving as it has been, not just in the context of the four or five things uttered a couple of paragraphs ago, but in light of a huge lesson for all. And to do this, I will share a story with you that I hope somehow, someway, delivers the message with clarity. Jump on into the Dividend Cafe …

The ABC’s of Exercise in my Life Story

I have written in the Dividend Cafe before of my practice around exercise – my view of trade-offs, my love of food, and why, for mental and physical health reasons, I do make myself exercise five times per week (it was more during quarantine). When I was in high school, I could eat anything I wanted and not gain a pound, much to the chagrin of someone trying to put on weight to avoid getting pushed around like a rag-doll in the key (I was the starting point guard on my high school basketball team, and let’s just say I was not the force of brute strength I would have liked to be). I ate and ate and ate and could not gain weight. Well, there is good news, and there is bad news now. I no longer “struggle” with that “problem.” Thirty years later, it turns out when I eat; I can gain weight. The bad news – my need for that extra size as I post up is, ummmm, nill. I retired from basketball at my first knee destruction over 20 years ago, and I am more likely to be running away from a bear these days than I am running up and down a basketball court (it makes me sad to write this).

So like many people, as the decades have gone by, I now have to work on diet and exercise to avoid gaining weight, and as someone who wears a suit every weekday of my life, I more or less refuse to get to a place of my suits not fitting me. I am a happily married guy, and I think my wife likes me, but when the suits are feeling a bit uncomfortable, I know things are slipping with the diet and exercise.

But I used the term “mental health” a moment ago as well, and I do think this is equally important to where I am going. Really, the physical part of controlling weight is far, far, far more diet-centric than exercise-centric, and it sure seems to me we’d all be better off to just face that music than keep denying it. If I ran ten miles longer than I do, it wouldn’t help me as much as avoiding fast food does. I need the physical exercise to motivate me to behave on the diet (I am an “all in” or “all-out” person, period), but scientifically, food intake trumps exercise many times over when it comes to real weight control.

But the benefits of exercise, for me at least (and I am sure many of you), is the mental, emotional, and even spiritual respite it can create. During the quarantine months of March/April/May and all of the intense, daily, somewhat indescribable grind that represented in markets, I made myself exercise every single day, seven days a week, no matter what – just to keep myself from a mental breakdown. I would work in my home study from 3 am-6 am every single day, and just spring up to go run the neighborhood or back bay as soon as the sun came up, and then get back to the house with a little recharge and reboot, every morning. It was an exponentially more productive and healthy habit than I recall the fall of 2008 being, where exercise was thrown out the window because of the anxiety of the financial crisis, and my sleep, diet, and workout habits all deteriorated.

So while I may not always look like it to you, I do exercise regularly and truly value the mental benefits it represents as a stress release, as well as the role it plays in reasonably containing my ability to fit in my suits.

Okay, well, what in the world does this have to do with present market levels?

Exercising the Need to Exercise

Four years ago, when we took our first apartment in New York City, I joined the club atop the Peninsula Hotel in midtown Manhattan as the place I would work out. It was about halfway between my apartment and my office, so I could walk there each morning, have a workout and a place to get ready, and use the space there to do serious reading/writing after my workout before heading into the office. It was a lovely setup, but since I re-opened my office in New York City five months ago, the Peninsula has remained closed (with plans to re-open in spring 2021). So right off the top, my primary option has been closed here in New York City.

Our new office building in the city (the Graybar Building at 44th & Lexington Avenue next door to Grand Central) has an Equinox touching it. While Equinox had been closed for months, they re-opened a while ago, and I ran in to join so it would serve as my “until the Peninsula re-opens” option for daily exercise. My condition when joining was that after my workout and getting ready each day, I needed a place to sit where I could read and write – my daily routine for which there is no flexibility. They have not only since taken that space out, but because of various city issues and incidents, their access, process, and feasibility of use has been impossible. My time there lasted a month. It was not a good experience.

My apartment building on the west side of Central Park has a lovely club on the top floor that I am happy to make my workout destination. They re-opened a couple of months ago (requiring a reservation and such but open nonetheless). However, early this week, they sent out a bulletin that they would be closed for a “thorough cleaning” – and apologized for the inconvenience. Things are re-opening now, but the home base option was out earlier in the week as they did a little housekeeping.

My preferred vehicle for exercise since I became more faithful with doing so is a thing called Orange Theory Fitness, a studio class that can be found all over the country where you basically are part of a group doing circuit training with an instructor, part treadmill, part rower, and part floor (weights, strap, etc.). It is a brutal workout, and I have learned to love it. The one I frequent in Newport Beach has re-opened, and when I am there, I absolutely love doing the 5 am class. But here in New York City, it is not so easy. The studio is sort-of open, but group classes are forbidden, and of course, masks are strictly required.

And now we are getting closer to the market lesson in this.

I went to Orange Theory this Monday morning at 5 am here in New York City because the Peninsula is closed, and because the Equinox option did not work, and because the club at my apartment building was shut down. I had a mask, but it had a small tear in it, and the club would not let me work out there (and didn’t have an extra mask for me). I had no other option now. It was absolutely freezing outside. Now, 30 degrees may not be very cold to many of you, but (a) It is cold to this born-and-raised Californian, and (b) The wind that comes off of the Hudson River in Manhattan’s upper west side is enough to make 30 degrees feel like 10 degrees. And yet, freezing, face fully numbed, joints hurting, this 46-year old worn-and-torn investment advisor found himself running Central Park in weather like this when the sun came up.

And this is the reason for the long set-up around various gyms and clubs and disappointments and broken down options …

I ran Central Park in 30-degree weather this week because the Peninsula is closed, Equinox was a bust, my apartment club was closed, and Orange Theory booted me for a tear in my mask.

I ran Central Park in miserable cold weather because I had no other option, yet I really wanted to exercise.

Tying this all together

Capital has a relentless need to be put to work. Investors have an insatiable need to get a return on their capital. Those two things are not subject to suspension (let alone debate) – they are laws of the universe. The worst expression ever concocted is “money under the mattress” – because it allows people to apply a mental image that might, maybe, sort of be possible for a small part of their personal finances (i.e., hiding a couple of thousand dollars of cash under the bed) – to global capital markets.

News flash: There is no global bed, or global mattress, for the world’s global capital to hide under. There are trillions upon trillions of dollars circulating in the universe, and they have to go somewhere.

Yes, some money can go into a money market. Some money can go into bank deposits. Some money can go under the mattresses of Mr. Smith and Mrs. Jones. But across the vast and complex and myriad owners of capital around the world, there exists a relentless need for a return on that capital. Income has to be generated. Growth has to be achieved. Insurance companies and pension funds that have actuarial commitments in the future put an expected rate of return on today’s dollars so that future dollars can meet those commitments. If that return does not materialize, guess what? Those commitments will not be funded. Endowments and Foundations have to give out charitable distributions, and they have to obtain a return on capital to find such. Governments and sovereign wealth funds seek to fund their long term liabilities with some return on their long term assets.

It is never going to change. Different economic actors, with different economic goals and circumstances, are moving at a million miles per hour, with a glut of capital tied to them seeking its most appropriate and efficient use. And to complicate things further, with interest rates at 0%, and the Fed balance sheet at $7 trillion (which ends up on bank balance sheets as excess reserves), there are all the normal realities I am describing at play, with a super-charged level of liquidity and flow of credit enhancing this reality.

Capital abounds, and it needs a place to go.

And when all four of your possible gym options fail to materialize, you have to run Central Park in 30-degree weather.

Translation: when money has to find a home, and interest rates are at 0% in domestic cash markets, and interest rates are negative in foreign cash markets, and bonds are hugging the zero-bound in yield, and international equities are subject to significant currency or fundamental risk, it is simply not that hard to see why for so many of these global dollars circulating around planet earth, the U.S. stock market becomes the best place to park the funds. Is it perfect? I mean, is the 30-degree weather exactly what all these economic actors want? Probably not. But they’ve deemed it their best option.

Not a perfect option. Not a risk-free option. Not a comfortable option. But for the circumstances in which they find themselves, their best option.

In summary

There is more capital than ever looking for a home.

That capital needs a best and optimal use more than ever (pensions are underfunded, etc.).

The various alternate options are now non-options (negative and zero interest rates).

Equities become the best available option for investors, drawing more capital in as the relatively predictable earnings streams represent a superior option to the other places capital could go.

It is policy-driven. And it is economic-related. But it is the lay of the land.

“There is no alternative” (TINA) is not an illegitimate investment explanation – it makes perfect sense, even if it is not ideal.

And oh yeah, one can even get a leg-up on the TINA explanation for capital allocation by being more selective, more prudent, and more focused on, well, dividend growth. But I digress …

***********************

A few other things I wanted to cover this week …

Midstream exceptions

(“Midstream” refers to the transportation and storage of oil and gas; it is “upstream” when it is being explored, drilled, produced; it is “midstream” when it is out of the ground and being moved or stored; it is “downstream” when it is at the refinery or otherwise being prepped as a finished product)

On the one hand, there is no question the entire energy sector has rallied in the last month or so and that commodity prices themselves have enjoyed a sentiment reversal (with oil prices seeing ~$45 vs. the spring’s range of $25). However, the price of oil has rallied before without midstream participating, and even in this oil rally, natural gas prices have stayed around $2.50. What has played out is a value stock “discovery and rotation” that midstream has participated in – for good reason. And from a fundamental standpoint, through all of the challenges of the COVID moment and the grind that has taken place since, the midstream sector has seen many companies (the ones intending to survive and thrive) get their capital spending plans in line, optimize distributions, and take the post-2020 economic realities seriously. There is still plenty of competition in the sector, and leverage on the balance sheets of a typical midstream company is hardly conservative, but overall, the environment feels good right now.

There are still soooooooo many investors on the sidelines from midstream exposure that I have not a worry in the world of the space getting overheated and “too euphoric.” It could happen, and if it does, it will require action on our part, but it is just so rare to be able to invest in a space on the basis of fundamentals and cash flows, which embeds enough risk/reward dynamics as it is, and not be engulfed in concerns about overheated sentiment. All things being equal, many investors like being in spaces that experience irrational exuberance, and why not? But from the vantage point of fundamentalists like ourselves who are extremely cash flow conscious, we can’t really go there, and to be making our decisions right now purely around the rights and wrongs of the space (there are both), and not concerns around sentiment and flows – is almost liberating.

Not all price appreciations are created equal. Something going up because everyone loves it is different than something going up because its price and value fundamentals are improving. The latter is what we seek out because the former we can’t control. It is my opinion that the outcomes in the midstream space will be driven by the latter for many months to come and that sectors driven by the former will be, well, unpredictable.

Not if but why

Higher yields do not mean equities hurt. A steeper curve can help equities, and higher rates at the longer end of the curve when they reflect organic, healthy economic growth are a good thing. It is higher rates that reflect real inflationary pressures that hurt stock (multiples) and bonds. So the reason rates move matters. My fear is not higher rates; it is the inability to get higher rates because of compressed growth caused by the debt-deflation cycle.

Politics & Money: Beltway Bulls and Bears

- I am ready to place my bet that Congress will not get a lame-duck session stimulus/relief bill done. I was adamant about this prediction just after the election but started to believe it was on the horizon late last week and early this week as conversations started providing various political actors cover to get on board. But those talks seem to be falling apart, and I just believe this is another “fooled again” moment. We shall see.

- The electoral college formalizes things for the Presidency this Monday, the 14th.

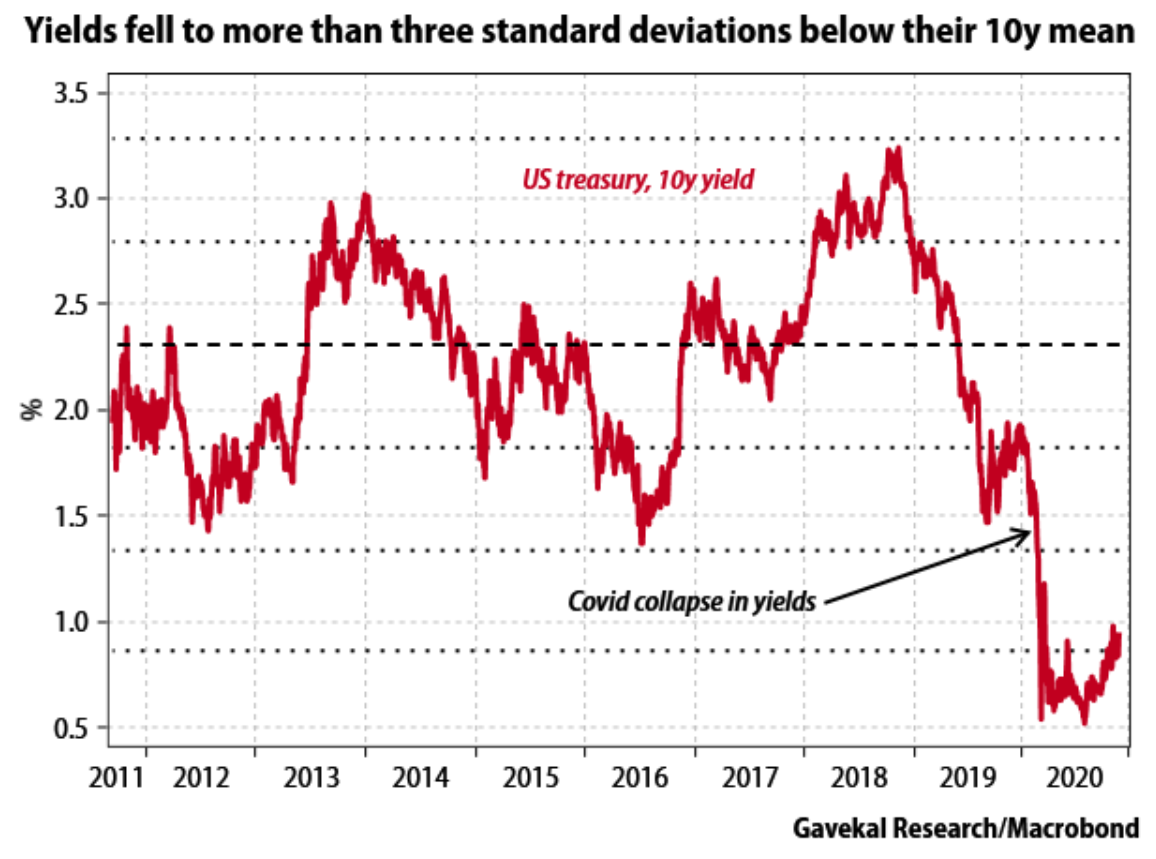

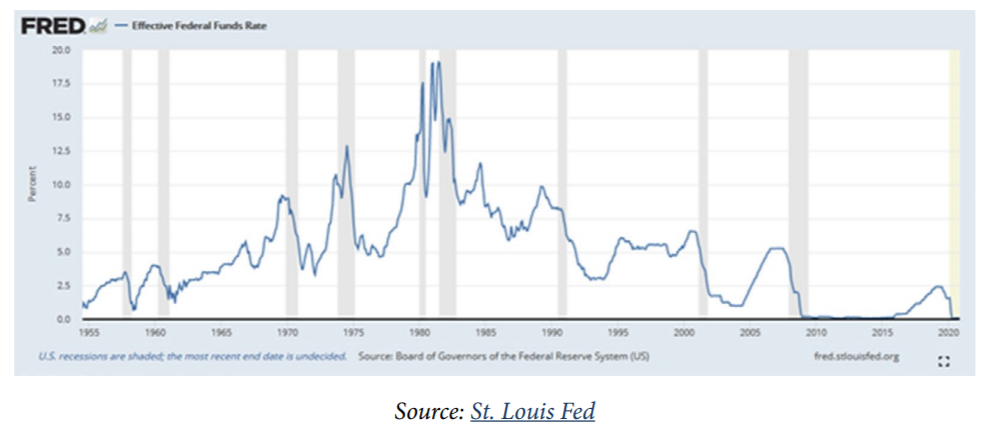

Chart of the Week

How bad are the options global capital is looking at, relative to equities? Take a look at the reality of ten-year treasury yields and the reality of the fed funds rate below that. Assets are priced against these things, and this is where we find ourselves.

Quote of the Week

“There is no bell that rings at the top, or bottom.”

~ Old Wall Street adage

* * *

If I annoyed you with my long set-up and talk of New York workout options this week, I apologize. For right or for wrong, the analogy came to me (while running, ironically enough), and I thought I would give it a shot. The underlying point is all that matters. Capital has to find a home, and we do ourselves a huge favor as investors to think about the realities of global capital more than we think about our own instincts and the daily headlines.

And with that, it is time to go for a run … Thank God my apartment club is back open! Thirty degrees is too cold. =)

This was my reward for staying diligent in the workouts this week (view out the window of the treadmill at my re-opened apartment fitness center).

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet