Dear Valued Clients and Friends –

I know what you all are thinking right now – “How could you even think about markets and the economy right now after that USC win over LSU on Sunday night?” – and I get it. But really, as much as I respect the obsession some of you have for USC football, for what appears to be a substantially improved defense, for a final-minute scoring drive for the ages, for two one-handed catches that will be catch-of-the-year candidates, and for all the things that make the Fight On spirit what it is… But look my friends, I have a job to do, and despite your constant requests for me to sit here and commentate about the game and the win over SEC powerhouse LSU, there are things happening in the world that warrant our attention. You’ll just have to forgive me for fighting on…

Dividend Cafe on Friday went around the horn to the state of the market, the state of the economy, some observations about the election, and more. The written version is here (my favorite), the video is here, and the podcast is here.

The market’s sell-off today was mostly behind a further correction in semiconductors and big tech, but also followed fundamental economic weakness as pertained to manufacturing. More below!

Off we go…

|

Subscribe on |

Market Action

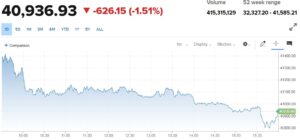

- The market opened down over a hundred points today, dropped a lot more thirty minutes later and then dropped more in the final two hours of trading.

- The Dow closed down -626 points (-1.51%), with the S&P 500 down -2.12% and the Nasdaq down a pretty nasty -3.26%.

*CNBC, DJIA, Sep. 3, 2024

- The market sell-off today will recalibrate a lot of the data points we brought into today (i.e., 35% of stocks were at 20-day highs – I assure you it is a lot lower now; 80% were above their 200-day moving average; I assure you that has dropped, too, but we’ll see how much tomorrow)

- One thing that I imagine has benefitted from today’s sell-off is the ongoing relationship between “even-weighted” and “cap-weighted” S&P indices. When the sell-off is concentrated in big-cap tech names, it drives the relative performance for “even-weight” higher, even if the total absolute performance is negative across the board.

- The ten-year bond yield closed today at 3.84%, down -6.7 basis points on the day.

- Top-performing sector for the day: Consumer Staples (+0.76%)

- Bottom-performing sector for the day: Technology (-4.43%) – undoubtedly affected by the -9.5% drop in Nvidia today (down -23.3% from its high)

- The challenge for many companies in big public markets is not their revenue or profit but the multiple being assessed by those. And with a company like Nvidia, the profit margin is so high that valuing earnings or revenues by assuming those margins are sustained is, shall we say, risky (the gross profit margin is currently 76%). As a multiple of sales, the current 25x is, well, much, much worse than the 65-70x earnings I frequently quote. And 18x next year’s astronomical revenue expectations are not exactly what we would call cheap.

Top News Stories

- Six hostages killed by Hamas were discovered in Gaza, one being an American, and several of them were alleged to be freed in terms of a ceasefire negotiation that had been under discussion.

Public Policy

- Vice President Harris came out against the sale of U.S. Steel to Japanese company, Nippon Steel. This unfortunate declaration mirrors the equally unfortunate declaration from the Trump campaign.

Economic Front

- The Q2 real GDP number came in at +3%, better than the +2.8% previously reported.

- ISM Manufacturing showed contraction once again (47.2 this month – anything below 50 is contraction) after a 46.8 last month. New Orders were the weakest since May of last year.

- Torsten Slok from Apollo sent a useful report yesterday on Chinese population demographics. We know population growth is negative, and we know that with a fertility rate of 1.0, this population trend is going to accelerate, dramatically, for decades to come.

Housing & Mortgage

- July pending home sales fell -5.5% on the month, as affordability continues to offset any other issues like high demand and economic fundamentals.

Federal Reserve

- Not a lot of changes this week in the futures market: there is a 67% chance of a quarter-point cut at the September meeting and a 33% chance of a half-point cut. There is a 100% chance of another quarter-point cut in the November meeting (the futures curve does not delineate between 25 in Sep./50 in Nov. or vice versa). There is a 71% chance that by December, we will be down a full percent (or more).

Oil and Energy

- WTI Crude closed at $70.41, down -4.27% to a new low in the year!

- Midstream energy was up +1.4% last week as oil was down, natty gas up, bond yields up, and the S&P barely up. Midstream’s correlation to everything has become very, very low.

- Howard Hinds pointed out, and this is fascinating to me – ten years ago, MLPs were over 60% of the midstream universe market cap; today, they are 35%. The C-corps and Canadians have grown in stature, and some MLPs have joined the C-corps via mergers and acquisitions (and conversions).

- Oneok (OKE) doing a $5.9 billion acquisition of EnLink and a $2.6 billion deal for Medallion, all the while rallying +5% higher, shows that sensible M&A with strategy (and preferably, accretive to earnings) can still be received well by the market.

Ask TBG

| “Why does QE and monetary inflation only affect asset prices (e.g., stocks, houses) and not real wages?” ~ Sergio |

| Monetary inflation DOES impact wages. QE does not because it does not get into the circulation of the money supply but stays “on the shelf” in excess bank reserves. |

On Deck

- The jobs report for August will come out this Friday, Sept. 6

To all a good night… and fight on!!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.