Enough?

If you are hosting a party, there is this natural anxiety about how much food to order, drinks to have, plastic ware to put out, etc. It’s this looming fear of running out.

Jesus’ first recorded miracle took place at a wedding celebration, in which they indeed did run out of wine. At this moment is when Jesus famously turns water into wine, allowing the party to go on.

It’s in our DNA. We are all wired with this itch or unsettling feeling of potentially showing up without enough; miscalculating our resources and not being able to fulfill our expectations.

Lions and Tigers and Inflation, Oh My!

In finance, inflation is this “not-enough” villain that’s always hiding in the shadows. We are good at figuring out how much stuff we can buy today; that mental math is easy. BUT this idea that our money loses its potency over time makes it very hard for us to figure out what we can afford tomorrow.

We are all looking for practical ways to combat the fact that a dollar is a dollar today, just as it is tomorrow, but a dollar will buy less today than it did yesterday and even less tomorrow (that’s a tongue twister). We are all in search of practical ways to hedge inflation.

Inflation is top of mind right now, and it’s everywhere we look these days – from newspaper headlines to political speeches to the gas prices at the pump.

Inflation Peeking

I take the same drive to work every day, and as that toll road starts its descent into Newport Beach, I get a clear view of the expanse that is the Pacific Ocean. What I see out there today is very different than what I would’ve seen two years ago. Today I see an ant farm of cargo ships lined up as far as the eye can see. This matches the articles I see in the Wall Street Journal regarding supply chain issues, ports being backed up, and all the other potential contributors to this recent spike in inflation.

The Dollar Dracula

As an advisor, I’ve spent a career trying to convince clients that inflation is a real risk factor that they need to account for in their financial plan. I’d often refer to it as the silent killer – the financial vampire – secretly sucking the value out of their money. For years, it’s been nearly impossible to engage an investor on this subject. Yet, NOW clients and prospective clients alike are VERY worried about inflation and eager to discuss the topic.

The media has instilled this inflation fear – as the media often likes to do – and investors don’t know practical steps to combat or defend against this vampire of finance. So, if you were looking for practical advice on combating inflation, you’ve come to the right place!

Let’s dive right in…

Fixed-Rate Mortgages

When thinking about inflation, we are always thinking about how expenses increase incrementally over time. So, if we want to create the most significant impact on combating inflation, we should start with strategies that address the largest expenses on our monthly budgets.

On average, folks typically spend about a third of their budget on housing. If one were to itemize their expenses into broad categories, housing would typically be their greatest expense. For a renter, housing expenses will inch up year by year as the landlord increases rent annually (inflation). One could sign a long-term lease, but typically a residential “long-term” lease will only help to lock in the expense for two or three years.

I look back at the first place my wife and I rented when we got married seven years ago. Today that same place is more than double the cost. That’s the financial vampire I spoke about; that’s inflation.

Buying a house is one practical hedge. Resourcing a 30-year fixed mortgage means that you get to fix (lock-in) your housing expense for a LONG time. I referenced the real-life example of what happened to rental prices over the last seven years, could you imagine what that jump looks like over 30 years?

A fixed-rate mortgage is an excellent inflation hedge.

Health Savings Accounts (HSAs) & 529 Plans

Sticking with this theme of focusing on top-of-the-food-chain expenses, let’s take a look at healthcare and education expenses. Two budget categories that have experienced rocket ship inflation in the last few decades are healthcare and education. So, two worthy inflation villains to address.

One of the best weapons for fighting inflation is to pay less in taxes. The more you keep in your pocket – as opposed to sharing with Uncle Sam – the further your dollar goes. The HSA and the 529 plan are two tax-friendly accounts aimed at covering healthcare and education expenses. Perfect, right?

You can and should chat with your financial advisor on ways to optimize these accounts – HSAs and 529s. I also suggest you listen to the Thoughts On Money podcast that we recorded to accompany this article, where my co-host, Sean Latimer, and I riff on this very subject.

The moral of the story is that planning ahead and investing in an HSA and/or a 529 can create meaningful future benefits and potentially create more buying power in the future instead of less.

Asset Allocation

I wrote an article earlier this year titled, An Inflation Irritation, and in this article, I addressed this fundamental financial exam question:

What is the best hedge against inflation?

(a) Bonds

(b) Cash

(c) Stocks

(d) Gold

Psst… the answer is “c” stocks. Why? Businesses can often pass increased costs onto the consumer, and their revenue growth is typically positively correlated to inflation. Remember, what is inflation? The rising prices of goods and services. Who sells these goods and services? Businesses. What are stocks? Micro ownership in those very businesses. Owning stocks puts you on the right side of the table if you intend on combating inflation.

Here is where asset allocation plays a significant role. Asset allocation is the investor’s strategic decision of what to own and how much to own of it. I know you have seen the pie charts; they have varying-sized slices that correlate to different percentages you own in stocks, bonds, cash, and alternatives. Some of these slices (e.g., stocks) will be a great hedge against inflation, while others (e.g., high-quality bonds) are sitting ducks waiting for the inflation fox to pounce.

Part of the TOM mandate is to help you mature as an investor. Finance 101 teaches you to measure investments according to their yield or interest rate or, perhaps even more broadly, their expected return. If you would like to graduate to the more advanced course, I’d suggest you start viewing all investments from the perspective of their “real” return. The financial measurement of a real return looks at an investment’s return net of inflation. In today’s current environment, many of the traditional fixed-income investments (government treasuries, Certificates of Deposit, Money Market savings, etc.) actually have an expected real return that is negative.

Riddle me this, if an advisor or banker sat you down and tried to pitch you an investment that had a high likelihood of producing a negative return for you, would you even entertain the idea for a moment? No way, right? What if I told you that there may very well be some allocations in your current portfolio that are just that. Don’t get me wrong; the advice isn’t just to run over and hit the sale button on all of your assets that have a negative expected real return. These investments could be suitable and appropriate; it all just depends on the objective. Low return or low-interest rate assets are meant to act as a reserve/safety net, and they are often included in a portfolio to help one weather a storm. One is willing to accept the low to negative real return on these types of assets, knowing that they (1) have other growth-bearing allocations elsewhere and (2) emergency funds need to have price stability and liquidity, which do not often co-exist with higher-yielding allocations. The question is how much of your current portfolio falls in this category? The answer to this question will determine how equipped you are to battle inflation.

Again, our last practical hedge is asset allocation. I encourage everyone to thoroughly review how your portfolio is designed, what those allocations currently look like, and what a reasonable person would expect the “real” return to be across those different investment types.

It’s Closing Time

I really can’t tell you how often the inflation conversation comes up these days. Let’s just say it’s a lot. I don’t put myself out there as some sort of macroeconomist, nor could I tell you with 100% certainty what exactly is causing these inflation spikes. Still, as a financial planner, I can give practical advice on addressing the inflation conversation.

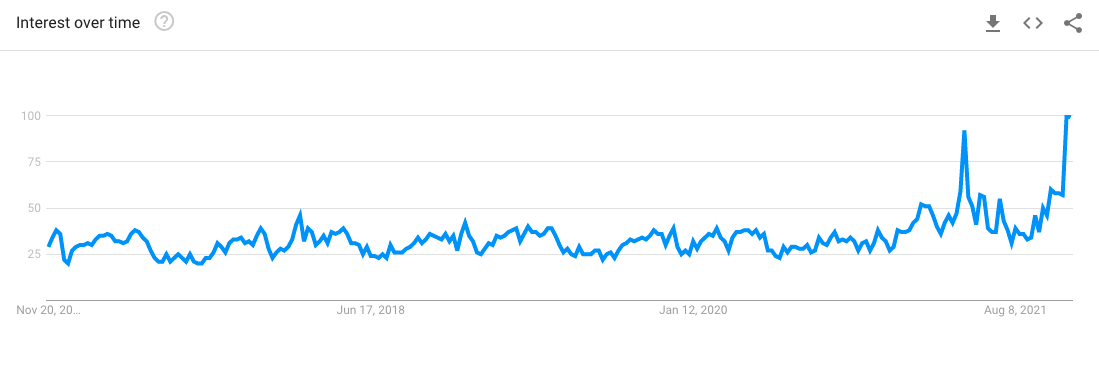

To further iterate this point, here is a snapshot of Google trends and the popularity of the word “inflation” versus the last five years:

*For Illustrative Purposes Only

Again, top of mind for a lot of folks right now.

I hope you found today’s discussion applicable and practical, as that was the intent. Remember, the theme is to address the most significant expenses first and see if you can’t put together a game plan to fend off inflation for those particular expenses. We all have unique approaches to budgeting, spending, and what things are most important to us. Take this opportunity to review your expenses and start crafting your strategy to combat inflation.

And that is all I have for you today. I wish everyone a wonderful Thanksgiving week, and I will be back post-holiday with more of my Thoughts on Money!